Is the Planet Fighting Back? Insurance in the Age of Climate Change: Challenges, Innovations, and a Sustainable Future

Global instability, the growing influence of artificial intelligence, and the questionable sustainability of planetary resources present new challenges for companies and individuals alike. Questions range from how to adapt to changes to whether existing ESG principles can adequately address these challenges. Understanding the potential risks involved in implementing ESG strategies is crucial to ensuring that business operations are sustainable and responsible toward the planet, people, and business.

Considering the climate changes that have shown us their “harsh face,” the question arises – is the planet fighting back? This was the central question during the open talk session at the fifth regional conference “Risks of the New Age: A New Era of Sustainability,” attended by Leo Pandžić, Head of Sustainability Department at DDOR.

On this occasion, Pandžić emphasized that insurance, although a traditional industry, is adapting to new living conditions due to climate change as it is inevitable that extreme weather events are becoming more frequent, leading to an increased number of claims.

“This reality demands constant updating of insurance practices and risk assessment models. Increased damages result in higher prices, making insurance less accessible. To strengthen resilience, the insurance industry relies on better risk management, portfolio diversification, innovation, and public-private sector cooperation. A significant portion of damages remains uninsured, burdening states and citizens, highlighting the need to improve risk management culture. A paradigm shift regarding the consequences of extreme weather events requires active involvement of insurance companies in developing measures to prevent damages,” said Pandžić, referring to Unipol’s ADA project, a tool developed to increase the resilience of the agricultural sector to climate change, which, using algorithms, will indicate current and future risks, as well as any possible actions that can be designed and implemented to address and limit farmers’ exposure.

When asked if abandoning polluter insurance in Serbia means a significant loss of premiums, given the increasing number of insurers who stop insuring polluters, Leo Pandžić replied:

“The decision to exclude environmental polluters and violators of human and labor rights from insurance is becoming an increasingly significant topic. Analyses have shown that close to 40% of corporate clients undergo ESG criteria, and less than 0.5% of them are excluded from insurance coverage. Due to the specifics of the insurance market in Serbia, the reactions of some insurers are slow. Although insurance companies do not directly pollute the environment, the risks they take on can have negative ecological consequences. The Unipol Group actively fights for environmental protection, aiming to reduce CO2 emissions by 50% by 2030 and create at least 30% of products with an E or S component in non-life insurance by the end of 2024. This practice demonstrates engagement in insurance aligned with sustainability goals.”

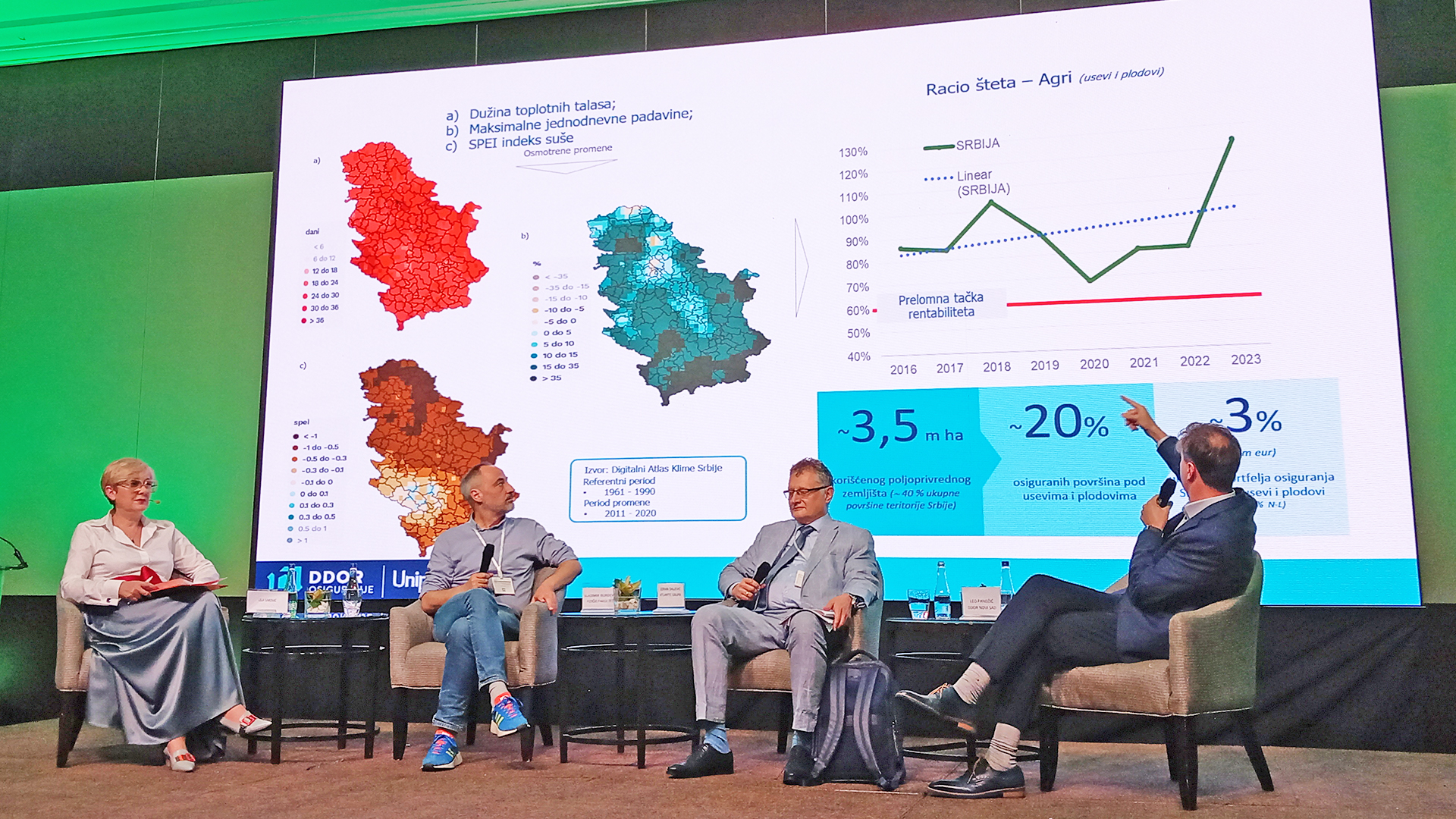

Pandžić also noted that insurers are facing increasingly frequent and costly damages resulting from climate change, raising the question of whether they will withdraw from providing insurance coverage. Examples such as StateFarm and AllState withdrawing from offering new homeowners insurance in California due to increasingly frequent and devastating natural disasters indicate a growing trend. Similar steps may be followed by other insurance companies, leading to rising insurance prices and related economic issues. In Serbia, crop insurance portfolios have been recording losses for years due to climate change, raising the question of when these effects will become the norm. Insurers are employing various strategies to protect against climate risks, including portfolio diversification and the use of advanced technologies and data to predict risks. More sophisticated prediction models need to be developed to adequately respond to new probability scenarios. Companies like DDOR and Unipol are intensively working on developing such tools to more effectively tackle future challenges.